Key takeaways

- The minimum interprofessional salary in Spain for 2026 is set at €1,221 per month, €40.70 per day, and €17,094 per year across 14 payments, under Royal Decree 126/2026.

- The increase represents a 3.1% rise on the 2025 figure, with retroactive effect from 1 January 2026, and is exempt from personal income tax (IRPF).

- Specific rates apply to temporary workers (€57.82 per legal working day) and domestic employees (€9.55 per hour), both updated under the same decree.

- Since 2018, Spain’s minimum wage has risen by a cumulative 66%, making it one of the fastest-growing minimum wage frameworks in the European Union.

New minimum wage requirements in Spain for 2026

Royal Decree 126/2026, of 18 February, establishing the Minimum Interprofessional Salary in Spain (Salario Mínimo Interprofesional, or SMI), was published in the Boletín Oficial del Estado (BOE) on 19 February 2026. The decree applies retroactively from 1 January 2026 through 31 December 2026, meaning employers who paid January wages at the 2025 rate are required to settle any arrears immediately upon publication.

The update follows a period of brief legal uncertainty at the start of the year. The government had initially extended the 2025 SMI via Royal Decree-Law 16/2025 of December 2025, but that extension was repealed by Congress on 27 January 2026. The Directorate-General of Labour issued interpretative guidance on 28 January 2026, confirming that no employer could reduce wages below the 2025 floor during the transition period, and that the eventual 2026 decree would carry retroactive effect from 1 January.

“The repeal of the extension does not imply the disappearance of the minimum interprofessional wage, nor does it authorise the establishment of salaries below the 2025 SMI.”

Directorate-General of Labour (DGT), Interpretative Guidance, 28 January 2026

The final 3.1% increase was agreed at the Social Dialogue table with Spain’s principal trade union confederations, CCOO and UGT, following negotiations in which unions had sought 7.5% and employer organisations had proposed 1.5%.

Minimum interprofessional salary in Spain 2026: the official figures

The minimum interprofessional salary in Spain for 2026 is established as follows under Article 1 of Royal Decree 126/2026:

- Monthly: €1,221.00 gross (in 14 payments)

- Daily: €40.70 gross

- Annual: €17,094.00 gross (including two extraordinary payments)

Only monetary remuneration is counted towards the SMI. Payment in kind may not, under any circumstances, reduce the full cash amount an employee is entitled to receive.

Since 2018, Spain’s minimum wage has increased by 66%, rising from €735 per month to €1,221 per month — an additional €485.10 per month, or €6,791.40 per year, for workers at the minimum floor.

Royal Decree 126/2026, BOE, 19 February 2026

Many Spanish contracts pay across 14 instalments per year, comprising 12 regular monthly payments plus two pagas extraordinarias — bonus payments typically made in summer and at Christmas. Some employers prorate these into 12 equal monthly payments instead, producing a gross monthly figure of approximately €1,424.50. The annual total of €17,094 remains identical under either structure. If you are uncertain which structure your contract uses, our labour law team in Valencia can review your employment contract and advise on compliance.

Regional context: minimum wage in Valencia 2026

The minimum interprofessional salary is a nationally uniform floor. The Valencian Community applies the same rates as the rest of Spain, with no regional derogation permitted below the statutory minimum.

- €1,221.00 per month in 14 payments per year

- €17,094.00 per year

- €40.70 per day

Valencia’s labour market is characterised by a strong presence of seasonal and hourly-paid workers across tourism, agriculture, hospitality, and logistics. These sectors employ a significant proportion of foreign workers and EU nationals whose contracts must respect the updated wage floor regardless of contract duration or type. For hourly-based part-time or temporary roles, the minimum wage in Spain per hour can be approximated at around €7.68, calculated by dividing the annual gross total by the standard legal working hours of approximately 1,826 hours per year.

Conditions for temporary workers in 2026

For casual or temporary workers whose cumulative services to the same employer do not exceed 120 days, the SMI is calculated on a daily basis and must include the proportional share of Sundays, public holidays, and the two extraordinary payments.

- Minimum daily rate (2026): €57.82 per legal working day

This rate represents a 3.1% increase on the 2025 figure of €56.08 per day. The same daily minimum applies to temporary and seasonal agricultural workers, a category of particular relevance across the Valencian Community’s fruit, vegetable, and horticultural sectors.

Conditions for domestic employees in 2026

Domestic workers paid by the hour — including external cleaners, carers, and household staff — benefit from a dedicated minimum hourly rate under Royal Decree 126/2026.

- Minimum hourly rate for domestic employees (2026): €9.55 per hour worked

This represents an increase of €0.29 per hour relative to the 2025 rate of €9.26. Employers of domestic staff are required to register workers with the Social Security system under the Special System for Household Employees (Sistema Especial para Empleados de Hogar) and pay contributions accordingly, regardless of the number of hours worked per week. Paying below the legal minimum — or failing to register domestic employees — exposes the employing household to inspection by the Labour and Social Security Inspectorate (Inspección de Trabajo y Seguridad Social, ITSS) and potential sanctions under the Law on Infringements and Sanctions in the Social Order (LISOS, Royal Legislative Decree 5/2000).

| Worker Type | Conditions | Minimum Rate (2026) | Change vs 2025 |

|---|---|---|---|

| Standard employees | Full-time, any sector | €1,221/month (14 payments) | +3.1% (was €1,184) |

| Temporary / casual workers | Services ≤ 120 days with same employer | €57.82 per legal working day | +3.1% (was €56.08) |

| Domestic employees | Hourly external household work | €9.55 per hour worked | +3.1% (was €9.26) |

| Part-time workers | Any duration, proportional hours | Pro rata of €17,094 annual | +3.1% proportional |

Minimum wage in Spain per hour for international students in 2026

International students studying in Spain under a student visa are permitted to work up to 30 hours per week during term time, in accordance with Organic Law 4/2000 (LO 4/2000) and Royal Decree 557/2011. The 2026 minimum wage rates applicable to student employment are as follows:

- For temporary or casual roles: €57.82 per legal working day (approximately €7.23 per hour based on an eight-hour shift)

- For domestic or household work: €9.55 per hour

Common part-time student roles — hospitality, retail, language tutoring, and administrative support — must comply with these rates or higher, as set by the applicable convenio colectivo (collective bargaining agreement) for the relevant sector. Students working in Valencia should ensure their employment contract explicitly states the gross hourly or daily rate and that the arrangement is correctly registered with the Tesorería General de la Seguridad Social (TGSS). Informal cash-in-hand arrangements carry legal risk for both the student and the employer.

The government estimates approximately 2.5 million workers will benefit directly from the 2026 SMI increase, of whom roughly two in three are women and a disproportionate share are under the age of 25.

Royal Decree 126/2026 Impact Assessment, BOE, February 2026

Self-employed workers: how the 2026 SMI affects autónomos

The minimum interprofessional salary does not apply directly to autónomos (self-employed workers), who set their own fees and remuneration. However, the SMI functions as a critical reference benchmark across several areas that affect self-employed professionals in Spain:

- Social Security contributions (cuota de autónomos): Monthly contributions are calculated on the basis of declared net income, with the minimum contribution base linked to the SMI as a reference threshold.

- Public subsidies and minimum income support: Eligibility criteria for programmes such as the Ingreso Mínimo Vital and many regional grants are expressed as multiples or fractions of the SMI.

- Digital Nomad Visa income requirements: The financial sufficiency threshold for the Digital Nomad Visa in Spain is set at 200% of the SMI for the principal applicant — meaning the 2026 requirement rises to approximately €2,442 per month.

- Tax deductions and thresholds: Various IRPF deduction thresholds and caps are referenced against the SMI, particularly in relation to tax planning for self-employed workers.

The 2026 SMI is entirely exempt from personal income tax (IRPF). Employees earning at or near the minimum wage level will not have income tax withheld from their payslip, though Social Security contributions continue to apply in the normal way.

Impact on employers and Social Security contributions

Employers must review their entire payroll to identify any employee whose total annual gross salary falls below €17,094 for full-time work and adjust wages accordingly. Part-time contracts are adjusted proportionally: a 50% contract requires a minimum gross of approximately €610.50 per month, and a 75% contract a minimum of approximately €915.75 per month.

The salary increase automatically lifts the minimum Social Security contribution base for affected employees, increasing employer costs beyond the gross wage rise itself. Employer Social Security contributions in Spain typically range from 30% to 39% of gross salary depending on the applicable category and contingency coverages, meaning the real cost per employee at minimum wage is considerably higher than the headline figure.

The Government of Spain has committed to reaching a minimum wage equivalent to 60% of the average national wage, in line with the criteria established by the European Committee of Social Rights. The 2026 SMI continues this trajectory.

Royal Decree 126/2026, BOE, 19 February 2026

Companies should also note that the government has indicated plans for a legal reform limiting the absorption of the SMI increase by existing salary supplements. Under current rules, employers may in some cases offset the SMI rise against absorbable supplements; forthcoming legislation is expected to restrict this practice significantly. Employers unsure of their obligations are advised to seek specialist labour law advice before the next payroll cycle.

Historical evolution of the minimum wage in Spain (2018–2026)

Understanding the trajectory of Spain’s minimum wage is important for long-term workforce planning, particularly for international businesses relocating UK employees to Spain or establishing Spanish operations for the first time.

| Year | Monthly SMI (14 payments) | Annual Total | Year-on-Year Change |

|---|---|---|---|

| 2018 | €735.90 | €10,302.60 | Baseline |

| 2019 | €900.00 | €12,600.00 | +22.3% |

| 2020 | €950.00 | €13,300.00 | +5.6% |

| 2021 | €965.00 | €13,510.00 | +1.6% |

| 2022 | €1,000.00 | €14,000.00 | +3.6% |

| 2023 | €1,080.00 | €15,120.00 | +8.0% |

| 2024 | €1,134.00 | €15,876.00 | +5.0% |

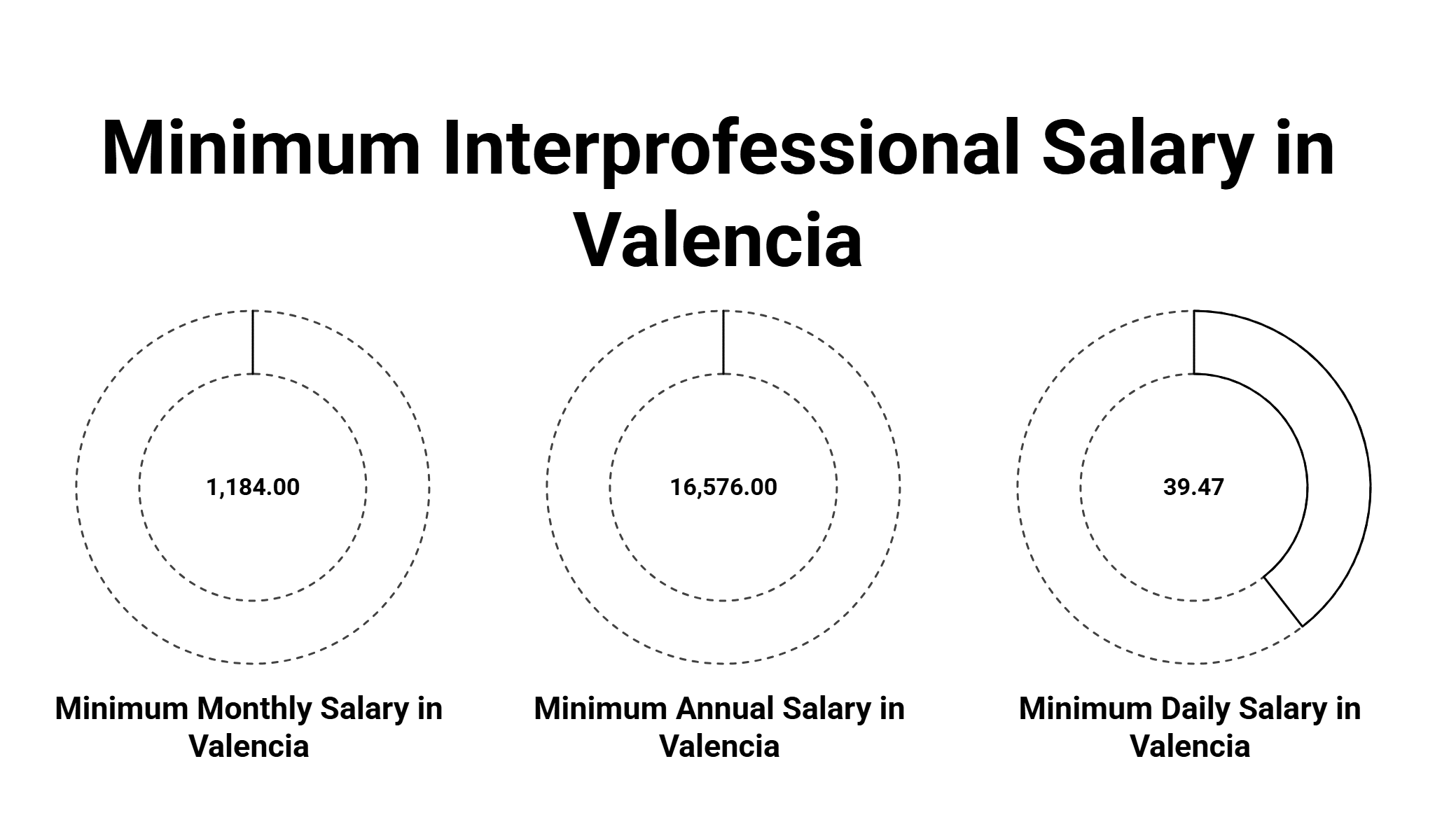

| 2025 | €1,184.00 | €16,576.00 | +4.4% |

| 2026 | €1,221.00 | €17,094.00 | +3.1% |

The cumulative increase since 2018 stands at 66%, reflecting the government’s commitment to the European Social Charter’s benchmark of approximately 60% of the average national wage.

Speak to our employment law team in Valencia

If you have questions about how the 2026 minimum interprofessional salary applies to your employment contract, payroll obligations, domestic employee registration, or self-employed income thresholds, our labour law specialists at De la Guía Luzón Abogados are available to assist you. We advise employees, employers, autónomos, and international clients in English, Spanish, French, and Russian.

Contact our legal team for personalised guidance on your case.

- Email: felix.delaguia@delaguialuzon.com

- Phone: +34 963 74 16 57

You can also reach us via our online contact form or explore our labour law services page for a full overview of how we support employers and workers in Spain.

Frequently asked questions about the minimum wage in Spain 2026

What is the minimum wage in Spain in 2026?

The minimum interprofessional salary (SMI) in Spain for 2026 is €1,221 gross per month, paid across 14 instalments, for a total annual gross of €17,094. The daily rate is €40.70. The increase was approved by Royal Decree 126/2026 of 18 February 2026 and applies retroactively from 1 January 2026.

Is the 2026 minimum wage subject to income tax in Spain?

No. Workers earning at or below the 2026 SMI are fully exempt from personal income tax (IRPF). Social Security contributions continue to apply in the normal way; the exemption is specific to IRPF withholding.

Does the 2026 SMI apply to part-time contracts?

Yes, on a proportional basis. Part-time workers must receive a minimum wage calculated in proportion to the hours worked relative to a full-time equivalent. A 50% part-time contract carries a minimum gross monthly salary of approximately €610.50, and a 75% contract a minimum of approximately €915.75.

What is the minimum wage for domestic workers in Spain in 2026?

Domestic workers paid by the hour are entitled to a minimum of €9.55 per hour worked under Royal Decree 126/2026. All domestic employees must be registered with Social Security under the Special System for Household Employees, regardless of how many hours per week they work. Failure to register exposes the employing household to sanctions from the Labour Inspectorate.

How does the 2026 SMI affect the Digital Nomad Visa income threshold?

The income sufficiency threshold for the Digital Nomad Visa in Spain is set at 200% of the SMI for the main applicant. With the 2026 SMI at €1,221 per month, the minimum monthly income requirement rises to approximately €2,442 per month. Additional requirements apply for accompanying family members: 75% of the SMI (approximately €915.75 per month) for a first dependent, and 25% (approximately €305.25 per month) for each subsequent dependent.

Do temporary workers have a different minimum daily rate?

Yes. Workers on fixed-term contracts whose total service with the same employer does not exceed 120 days are entitled to a minimum of €57.82 per legal working day. This rate includes the proportional share of Sundays, public holidays, and the two extraordinary annual payments. The same daily minimum applies to temporary and seasonal agricultural workers.

Can an employer offset the SMI increase against existing salary supplements?

Currently, Spanish law permits employers to absorb some of the SMI increase against absorbable salary supplements, provided the employee’s total remuneration does not fall below the new minimum. However, the government has announced a forthcoming legal reform designed to limit this practice. Employers should seek specialist labour law advice to assess how the absorption rules interact with their specific collective agreements before implementing any changes.

Does the autónomo social security contribution change with the new SMI?

The cuota de autónomos is calculated on the basis of declared net income, using a contribution base system reformed in 2023 and being phased in progressively. The SMI is used as a reference point for the minimum contribution base and for various subsidy and grant eligibility thresholds. If you are self-employed in Valencia and unsure how the 2026 SMI affects your contributions or tax obligations, contact us at felix.delaguia@delaguialuzon.com or call +34 963 74 16 57.

Is the minimum wage the same across all regions of Spain, including Valencia?

Yes. The minimum interprofessional salary is a national floor that applies uniformly across all autonomous communities, including the Valencian Community. Certain collective bargaining agreements (convenios colectivos) at sectoral or regional level may establish higher minimum rates than the statutory SMI, but no agreement can set a rate below it. Workers employed in Valencia in sectors covered by a convenio colectivo should verify both the SMI and the applicable sector agreement to determine which rate governs their contract.