Key takeaways

- Selling US investments to fund a Spanish property purchase can trigger US and Spanish tax implications.

- Owning Spanish real estate as a non-resident may create ongoing Spanish tax obligations (and the total can vary depending on where the property is located.

- When the property is sold, Spain’s 3% non-resident withholding mechanism and US worldwide income reporting rules must both be considered, with the Foreign Tax Credit often used to mitigate double taxation.

US and Spanish tax implications of using US investment money to buy Spanish real estate

What this scenario usually means (and what it doesn’t)

“Using US investment money” typically means you sell US investments (stocks, ETFs, mutual funds, etc.) in a US brokerage account, move the cash to Spain,

and then purchase Spanish real estate.

In most cases, the act of buying property is not taxable by the US itself, but the steps around it can create US and Spanish tax implications.

These include:

- US capital gains

- Spanish acquisition taxes

- Ongoing income/asset reporting in one or both countries.

Key principle:

Spain taxes income that comes from property located in Spain.

The United States taxes its taxpayers on their worldwide income.

To prevent being taxed twice on the same income, tax treaty rules and foreign tax credits may apply.

Residency status often drives the result.

Step 1: Selling US investments to raise cash (US-side taxation)

In general, capital asset dispositions are reported through Form 8949 and aggregated on Schedule D.

IRS guidance for Form 8949 confirms it is used to report sales and exchanges of capital assets,

with totals carried to Schedule D.

If the funds come from retirement accounts (e.g., an IRA/401(k)), the tax treatment can be very different (distributions and potential penalties).

If you are relocating or already living in Spain, retirement-planning decisions often overlap with residency and cross-border income reporting (see QROPS transfer to Spain for an example of pension-related cross-border planning considerations).

Important:

Be cautious with self-directed IRA strategies. Retirement account rules are complex, and mistakes can result in significant tax consequences and penalties.

Step 2: Moving money to Spain (US and Spanish tax implications)

FBAR (FinCEN Form 114)

If you are a “US person” for FBAR purposes and you have a financial interest in or signature authority over foreign financial accounts,

you generally must file an FBAR if the aggregate value exceeds $10,000 at any time during the calendar year.

Form 8938 (FATCA)

Form 8938 is for “specified foreign financial assets” above thresholds.

Importantly, the IRS explicitly states that foreign real estate itself is not a specified foreign financial asset required to be reported on Form 8938 (e.g., a personal residence or rental property).

That said, foreign accounts used in the process can still be reportable under FBAR/8938 depending on facts and thresholds.

If you also have income streams from other countries while living in Spain, those can create additional reporting layers (for a practical example, see how to declare UK income in Spain).

Step 3: Buying Spanish real estate (Spain-side acquisition taxes)

In Spain, the taxes at purchase typically depend on whether the property is resale or new construction, and the legal form of the transaction.

Two major categories are commonly encountered:

- ITP/AJD (Impuesto sobre Transmisiones Patrimoniales y Actos Jurídicos Documentados): A transfer/transaction tax framework established in national law and applied depending on the type of act.

- IVA (VAT): Applicable in certain circumstances (often new builds and specific developer sales), governed by Spain’s VAT law.

Note: The exact rate you pay can depend on region, property type, and transaction details; regional differences can be significant (see Spain regional property taxes).

Also, budget for transaction costs beyond taxes (notary, registry, legal work, etc.).

Common touchpoints at purchase

| Event | Spain (typical obligation) | US (typical obligation) |

|---|---|---|

| Sell US investments to raise cash | Usually not a Spanish tax event unless you are Spain tax resident and the sale is within Spain’s tax scope | Capital gain/loss reporting (Form 8949 + Schedule D pathway) |

| Wire funds to Spain / open a Spanish bank account | Bank onboarding/compliance (not an income tax by itself) | Potential FBAR if foreign accounts > $10k aggregate; possible Form 8938 if thresholds met |

| Buy Spanish property | ITP/AJD or IVA framework applies depending on the transaction | No “purchase tax,” but keep records; foreign accounts may be reportable |

If you are buying through a company or considering a corporate structure, the tax analysis can change.

Step 4: Owning the property (Spanish income taxes can apply even without rent)

Spain has specific rules for non-residents who own Spanish real estate.

The tax regime most often involved is the Impuesto sobre la Renta de no Residentes (IRNR), which taxes income obtained in Spain by non-residents.

Non-resident “imputed income” on urban property used personally

If you are a non-resident and you own an urban property for your own use (not rented), Spain can apply an imputed income concept.

The Spanish tax authority explains the calculation method as generally 2% of the cadastral value, or 1.1% in certain cases, with details provided in their guidance.

You can do this with the AEAT “Cálculo de la renta imputada”

If you rent it out: IRNR rental income reporting (Model 210)

Rental income from Spanish real estate is generally taxable in Spain, and AEAT provides a dedicated IRNR framework and filings.

Model 210 is used to declare different kinds of non-resident income (including rental income and imputed income).

AEAT also publishes reference rates for IRNR in certain contexts and explains that EU/EEA residents may have different rates than others.

If you’re trying to optimise your overall Spanish tax position (while staying compliant), see how to reduce your tax burden in Spain.

Wealth tax exposure (situational)

Spain also has a wealth tax (Impuesto sobre el Patrimonio) that can apply to individuals (including non-residents) depending on facts, and AEAT provides filing/obligation guidance.

Step 5: Selling the property (Spain withholding + gain reporting; US capital gain reporting)

Spain: 3% withholding mechanism when a non-resident sells

If the seller is a non-resident, Spain has a specific mechanism where the buyer must withhold and pay 3% of the agreed price as a payment on account of the seller’s tax.

AEAT states this explicitly and indicates the payment is made via Model 211.

Spain: Capital gains filing under IRNR

The seller typically reports the actual gain under IRNR rules using the appropriate non-resident return structure (commonly Model 210),

with AEAT providing a dedicated page for “ganancias patrimoniales derivadas de la venta de inmuebles.”

US: Worldwide income + reporting the sale

For US taxpayers, selling foreign real estate can create a US capital gain that is reportable on the US return (commonly through Schedule D/Form 8949 workflows).

IRS guidance confirms Form 8949 is used to report sales/exchanges of capital assets and is filed with Schedule D.

If your situation involves multiple jurisdictions, treaty/credit planning is usually a core part of the analysis.

How double taxation is usually reduced (treaty + foreign tax credit)

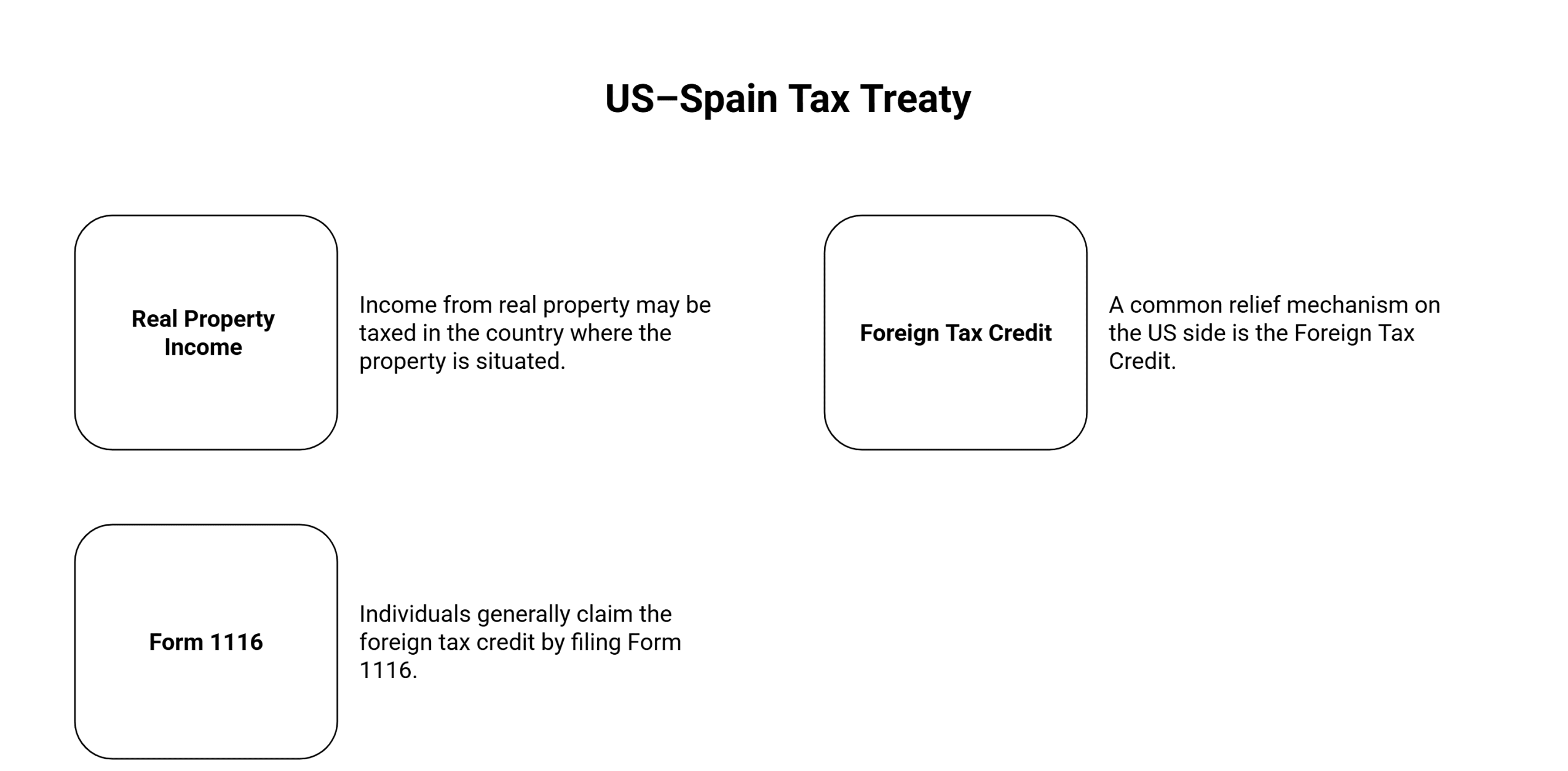

The US–Spain income tax treaty framework allocates taxing rights in important areas.

For example, treaty language confirms that income from real property may be taxed in the country where the property is situated.

On the US side, a common relief mechanism is the Foreign Tax Credit.

The IRS explains that individuals generally claim the foreign tax credit by filing Form 1116 (with limited exceptions).

If you are signing purchase contracts, loan documents, or cross-border agreements tied to the investment, legal drafting and review matters.

Mini case study: US and Spanish tax implications explained

Scenario: A US taxpayer sells US ETFs to fund a €500,000 resale apartment in Spain (non-resident owner), opens a Spanish bank account to complete the purchase,

uses the apartment personally for part of the year, and later rents it out.

What typically happens

- US investment sale: The ETF sale can create a US capital gain, reportable via Form 8949/Schedule D mechanics.

- Spanish bank account: The Spanish account may become reportable on the FBAR if aggregate foreign accounts exceed $10,000 at any time.

- Spain purchase taxes: The resale purchase usually sits in the ITP/AJD framework in national law (and the total can vary by region—see regional property taxes).

- Owning without rent: Spain may apply imputed income rules to an urban property held for personal use, based on the cadastral value and percentages described by AEAT.

- Renting it out: Spanish rental income is declared under IRNR mechanisms; AEAT provides Model 210 as the key filing for non-resident income categories.

- US relief: If Spain taxes the rental income/capital gain, the US Foreign Tax Credit (Form 1116 in many cases) may help reduce double taxation.

Compliance checklist (high-level)

| Topic | US-side items (common) | Spain-side items (common) |

|---|---|---|

| Foreign accounts | FBAR when aggregate foreign accounts exceed $10,000 at any time (FinCEN 114) | Local bank compliance (not an income tax filing by itself) |

| Owning for personal use | Recordkeeping; Form 8938 does not require reporting the real estate itself | Possible IRNR “imputed income” methodology based on cadastral value |

| Renting out | Report rental income/expenses on Schedule E framework (IRS guidance) | IRNR declaration via Model 210; IRNR rates depend on status |

| Selling | Capital gain reporting (Form 8949/Schedule D path) | 3% buyer withholding via Model 211 when seller is non-resident; seller gain filing via IRNR guidance |

| Double-tax relief | Foreign Tax Credit frequently via Form 1116 | Treaty allocates taxing rights (real property income taxable where situated) |

If you’re in Spain under a specific immigration status, it can affect your practical planning timeline and residency analysis:

Professional legal support for US and Spanish tax implications

Contact Delaguía y Luzón today to receive clear, strategic advice on the

US and Spanish tax implications of purchasing Spanish real estate with US investment funds, including

non-resident tax filings, cross-border reporting obligations, and double taxation considerations.

- Email: felix.delaguia@delaguialuzon.com

- Phone: +34 963 74 16 57