Limited Company in Spain: Key Takeaways for 2026

- A limited company in Spain can still be incorporated with share capital from €1, although founders should still choose a realistic capital figure for banking, credibility, and early operating costs.

- The CIRCE/DUE route is often the fastest option for many SL incorporations, especially when the structure is straightforward and the documentation is ready.

- Incorporation is only the start: after signing before a notary, you still need tax registration, a definitive tax ID, accounting setup, and possible Social Security registrations.

- The best structure depends on your activity, residence, and tax profile, so incorporation should be aligned with matters such as residency in Spain, VAT treatment, and long-term tax planning.

Starting a limited company in Spain in 2026: Key considerations for entrepreneurs

Are you planning to start a business in Spain in 2026? If so, one of the most common structures to consider is the limited company in Spain, known locally as a Sociedad Limitada or SL.

It remains the preferred option for many founders, freelancers moving into a company structure, family businesses, and foreign investors who want limited liability, a more formal corporate image, and a clearer separation between personal and business assets.

In practical terms, creating a limited company in Spain is more flexible than it used to be, but it is not something to treat as a simple formality.

The legal form may be easy to incorporate, yet the wrong articles, poor tax classification, or a rushed setup can create problems later with partners, invoicing, payroll, or cross-border taxation.

That is why the question is no longer just “how do I register a company in Spain?” The better question in 2026 is whether an SL is really the right vehicle for your business model, expected turnover, shareholder structure, and tax residency position.

This is especially important if you are also reviewing Spain corporate tax, comparing self-employment with an SL, or planning for a move to Spain with business activity already running abroad.

What is a limited company in Spain?

A limited company in Spain is a separate legal entity that can trade, hire staff, sign contracts, and hold assets in its own name.

In general, the liability of the shareholders is limited to their contribution to the company, which is why the SL is usually the go-to structure for small and medium-sized businesses.

For many founders, an SL works well when there will be more than one shareholder, when commercial risk is higher, when a stronger corporate image is needed, or when the business is expected to grow beyond a simple sole-trader model.

It is also often worth considering if you need to enter into international contracts in Spain or if you want a clearer structure for future investment, succession, or sale.

How to register a limited company in Spain in 2026

Spain still allows company incorporation through the standard route and through the CIRCE system, which centralises many formalities through the DUE (Documento Único Electrónico).

For straightforward cases, CIRCE can save time and reduce duplication, which is why it remains highly relevant in 2026.

| Step | What happens | Main result |

|---|---|---|

| 1. Company name clearance | You reserve a unique company name and check availability. | Name clearance certificate |

| 2. Drafting the company rules | You prepare the articles of association and decide on shareholders, directors, address, and business activity. | Incorporation documentation |

| 3. Share capital | You evidence the initial capital contribution and define ownership percentages. | Capital contribution support |

| 4. Notary signing | The deed of incorporation is signed before a Spanish notary. | Public deed |

| 5. Tax registration | The company is registered with the Tax Agency, usually through Model 036. | Provisional tax ID and census registration |

| 6. Mercantile registration | The company is registered in the relevant Mercantile Registry. | Full legal incorporation |

| 7. Post-incorporation compliance | VAT, accounting, payroll, Social Security, and tax obligations are activated as needed. | Operational company |

1. Company name and initial planning

The first practical stage is choosing the name of your limited company in Spain. This should be done carefully, not only to ensure availability but also to avoid later branding or contractual issues.

It is sensible to prepare several alternatives in order of preference.

At the same time, founders should settle the real commercial points before any filing starts: who the shareholders will be, how many directors there will be, whether directors act jointly or individually, what business activity codes apply, and whether the registered office and management will genuinely be in Spain. These are not minor details. They affect tax residency, corporate governance, and liability.

2. Share capital: what changed and what still matters

One of the biggest changes in recent years is that an SL can now be incorporated with share capital from €1, replacing the old €3,000 minimum. That reform is still in force in 2026 and is one of the reasons why creating a company in Spain is now more accessible for startups and smaller projects.

Still, founders should think beyond the legal minimum. A company with very low capital may look weak to suppliers, landlords, or financial institutions.

It can also create an immediate need for shareholder loans or further funding. For that reason, many businesses still incorporate with a more practical level of capital even though the law now allows less.

3. Articles of association: the step that should not be rushed

The articles of association are the backbone of your SL. They define how the company is managed, how decisions are taken, what powers the directors have, and how ownership is structured.

Standard wording may work for a simple one-shareholder company, but many businesses need something more tailored.

If there are multiple founders, foreign shareholders, or future investment plans, this document should be drafted with care.

It is often the difference between a company that works smoothly and one that generates avoidable conflict later.

This is also the right stage to think about related issues, such as how to reduce your tax burden in Spain without creating structural mistakes from the start.

4. Notary signing and public deed

Once the documents are ready, the incorporation deed is signed before a Spanish notary. This is what turns the private arrangements between founders into a public legal act.

The deed usually includes the company name, shareholder details, director appointments, business purpose, registered office, and the articles of association.

After this point, the company begins to take legal shape, but it is not yet fully operational for all purposes.

A common mistake is to assume that the notary appointment means the process is finished. In reality, several tax and registration steps still follow.

5. Tax ID, Model 036, and tax census registration

After signing, the company must be registered with the Spanish Tax Agency.

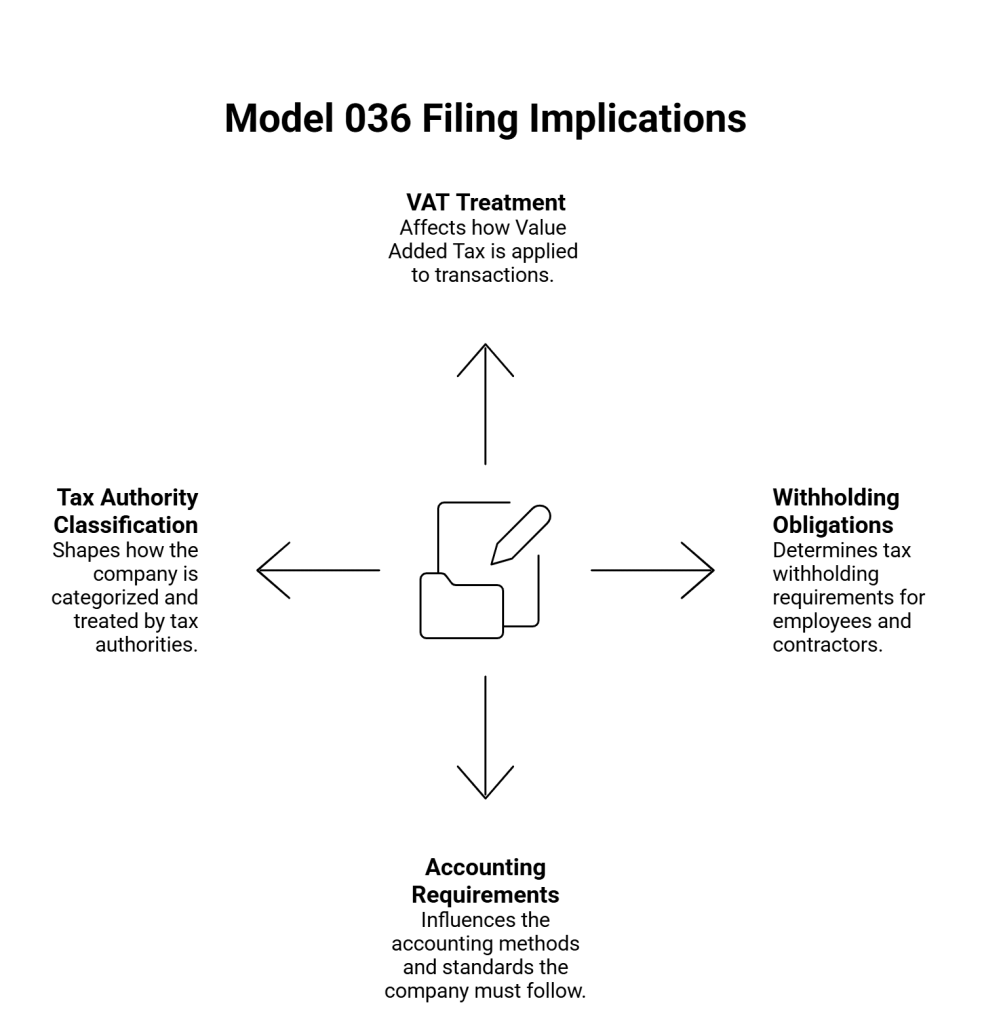

In practice, this usually means filing Model 036 so the company can enter the census of business taxpayers and obtain its tax identification details. This is also where the company formally declares the beginning of activity, tax obligations, and VAT position, where relevant.

This stage is more important than it sounds. Model 036 is not just a box-ticking exercise. The selections made here can affect VAT treatment, withholding obligations, accounting requirements, and the way the company is classified by the tax authorities.

If your activity may be exempt or partially exempt, it is worth reviewing the VAT exemption in Spain before filing.

6. Mercantile registration and definitive tax ID

The next stage is registration of the company in the relevant Mercantile Registry. Once this is completed, the SL becomes fully incorporated.

The company should then move from the provisional tax ID stage to the definitive one within the applicable timeframe.

Even though the core process is now faster than it was years ago, founders should still allow time for document review, identity checks, translations where necessary, and post-notary registrations.

Straightforward cases move faster; more complex shareholder structures do not.

Process chart: setting up a limited company in Spain

What taxes does a limited company in Spain pay in 2026?

Many founders assume that once the SL is registered, tax becomes simpler. In reality, a company structure creates a different compliance profile, not necessarily a lighter one.

In 2026, the general corporate income tax rate remains 25%, while newly created entities carrying out economic activities may benefit from a 15% rate in the first tax period with a positive taxable base and the following one, subject to the applicable conditions.

There are also reduced-dimension and microenterprise rules that may matter depending on turnover and taxable base, so the right reading is not just “company tax is 25%.”

It depends on the company’s size, timing, activity, and tax profile. Founders should also track filing dates from the beginning, which is why it helps to review the main Spanish tax deadlines early rather than waiting for the first year-end.

| Post-incorporation area | What to check |

|---|---|

| Corporate tax | General rate, new-company rules, accounting profit vs taxable profit, year-end filing obligations |

| VAT | Whether the activity is taxable, exempt, partly exempt, domestic, EU, or cross-border |

| Payroll and withholdings | Director remuneration, employee salaries, withholding obligations, filings, and records |

| Accounting | Bookkeeping, annual accounts, invoice control, and supporting documentation |

| International exposure | Double taxation, permanent establishment risk, and foreign shareholder implications |

Do you need Social Security registration?

Yes, often. If your company will hire employees, employer registration with the Spanish Social Security system is required before the activity begins, and employee registrations must be completed before the employment relationship starts.

This is a separate compliance track from tax registration and should not be left until the last minute.

In addition, in some cases, shareholder-directors or working partners may also need to be registered under the appropriate Social Security regime, depending on their role and control of the company. This is one of the areas where founders most often need tailored advice, because the answer depends on the specific structure rather than the company form alone.

When an SL makes sense for expats and international founders

A limited company in Spain can be an excellent option for expats and international founders, but only when it fits the wider legal and tax picture.

If you are moving to Spain while keeping foreign income, business interests, or directorships abroad, the structure should be reviewed together with your personal tax residence and reporting obligations.

This is particularly relevant if you are comparing your company setup with issues such as US and Spanish tax implications or need to declare UK income in Spain.

In other words, incorporating a company in Spain is not just a commercial step. For many foreign residents, it is also a cross-border legal and tax event.

Practical checklist before you incorporate

[ ] Confirm whether an SL is better than operating as self-employed [ ] Decide the shareholders, percentages, and director structure [ ] Define the real business activity and tax treatment [ ] Prepare the articles of association carefully [ ] Structure initial capital realistically, not just legally [ ] Plan Model 036 and VAT classification properly [ ] Check whether Social Security registrations will be needed [ ] Set up accounting, invoicing, and compliance from day one

Final thoughts on setting up a limited company in Spain

Setting up a limited company in Spain is more accessible in 2026 than it was a few years ago, especially thanks to the possibility of incorporation with €1 capital and the continued use of the CIRCE/DUE route.

Even so, the legal incorporation itself is only one part of the process.

The real success of the structure depends on whether the company is set up correctly for tax, governance, payroll, and future growth.

If you want your SL to be efficient from the beginning, the focus should not only be on speed. It should be on getting the structure right, avoiding costly corrections later, and making sure your company fits your personal and commercial circumstances from day one.

Need tailored help with shareholder structure, tax setup, or cross-border issues when creating a company in Spain?

Professional support for setting up a limited company in Spain

Contact Delaguía y Luzón today for tailored advice on

limited company formation in Spain, including company structuring, tax registration, and ongoing compliance for both residents and international founders.

- Email: felix.delaguia@delaguialuzon.com

- Phone: +34 963 74 16 57

Frequently Asked Questions: Limited company in Spain

What is the minimum share capital to set up a limited company in Spain?

Since the recent reform, a Sociedad Limitada (SL) in Spain can be incorporated with as little as €1 in share capital, replacing the old €3,000 minimum. However, founders should not confuse the legal minimum with the practical minimum. If the company needs early liquidity, deposits, stock, or payroll from day one, a more realistic capital figure is usually advisable to maintain credibility with banks and suppliers.

How long does it take to register a limited company in Spain in 2026?

The timeline depends on the complexity of the structure. Straightforward cases using the CIRCE/DUE route tend to move faster, as this system centralises many of the formalities. However, founders should still allow time for document preparation, identity checks, notary signing, tax registration via Model 036, and Mercantile Registry inscription. More complex shareholder structures or foreign shareholders typically take longer.

What taxes does a limited company in Spain pay?

In 2026, the general corporate income tax rate is 25%. However, newly created companies carrying out economic activities may benefit from a reduced 15% rate for the first tax period with a positive taxable base and the following one, subject to applicable conditions. Beyond corporate tax, the company will also need to manage VAT, payroll withholdings, and potentially other obligations depending on the activity and turnover.

Does a limited company in Spain need to register with Social Security?

Yes, in most cases. If the company plans to hire employees, employer registration with the Spanish Social Security system is required before the activity begins, and each employee must be registered before their employment starts. Additionally, shareholder-directors or working partners may also need to register under a specific Social Security regime depending on their level of control and involvement in the company. This is a separate compliance track from tax registration.

Can a foreign national or expat set up a limited company in Spain?

Yes, foreign nationals and expats can set up a limited company in Spain. However, the structure should be reviewed carefully, taking into account personal tax residency and any cross-border obligations. If you hold foreign income, serve on foreign directorships, or have business interests in another country, incorporating in Spain is not just a commercial step; it is also a cross-border tax and legal event. Specialist advice is strongly recommended to avoid conflicts with double taxation rules or permanent establishment risks.