Key takeaways

- Tax structuring between Ireland and Spain must reflect where the business is actually managed and where the owner is tax resident, not just where the company was originally incorporated.

- Personal tax residence and economic activity are key triggers in Spain, particularly under the 183-day rule and the “centre of economic interests” test.

- The Ireland–Spain double taxation treaty helps prevent double taxation, but does not replace the need for a properly aligned structure.

Tax structuring between Ireland and Spain

Tax structuring between Ireland and Spain has become a practical issue for founders, consultants and owner-managed businesses whose commercial centre is no longer in Ireland. Once the real activity, management decisions, invoicing flow or personal residence begins shifting to Spain, the original Irish setup may stop matching the tax reality. At that point, the question is no longer whether the Irish structure was efficient at the start, but whether it still fits the facts today.

Official tax comparison

| Area | Ireland | Spain | Why it matters in a transition |

|---|---|---|---|

| Corporate tax | 12.5% on trading income; 25% on certain non-trading income | 25% general rate; 15% for certain new entities in the first positive tax period and the next | The headline rate is only one piece of the analysis. The character of the income and the location of real management are just as important. |

| Standard VAT rate | 23% | 21% | Pricing, cash flow and invoicing workflows can change when moving from an Irish to a Spanish operating model. |

| Individual tax residence | 183 days in a tax year, or 280 days over two tax years, with a minimum presence rule | More than 183 days in Spain, or where the main nucleus or base of economic interests is in Spain | A founder can trigger Spanish tax exposure before formally restructuring the company. |

| Company tax residence | Irish incorporation can create Irish tax residence; central management and control remain relevant for foreign-incorporated companies | The personal residence rules focus on presence and economic interests; Spanish taxation also looks closely at where activity is really carried on | Keeping an Irish company while effectively managing the business from Spain can create a mismatch and added risk. |

| Corporate filing deadline | Return and payment are due by the 23rd day of the ninth month after the accounting period ends, when filed electronically | Return filed within 25 calendar days following the six months after the tax period ends | Moving to Spain changes the annual compliance calendar and often the accounting workflow too. |

| Default VAT filing cycle | Bi-monthly by default | Spanish filing deadlines are set through the taxpayer calendar and model-specific rules published by the Tax Agency | Compliance processes need to be rebuilt, not just translated. |

When an Irish structure stops matching the business

That does not automatically mean the Irish company must disappear.

However, it does mean the structure should be tested against the official residence rules. For individuals, Ireland uses the 183-day and 280-day residence tests, while Spain treats a person as tax resident where they spend more than 183 days in Spain or where the main base of activities or economic interests is located in Spain.

If the founder has already become a Spanish tax resident, the company structure needs to be reviewed alongside the owner’s personal position, especially around residency in Spain and the wider personal planning that follows a move.

That does not automatically mean the Irish company must disappear.

However, it does mean the structure should be tested against the official residence rules. For individuals, Ireland uses the 183-day and 280-day residence tests, while Spain treats a person as tax resident where they spend more than 183 days in Spain or where the main base of activities or economic interests is located in Spain.

If the founder has already become a Spanish tax resident, the company structure needs to be reviewed alongside the owner’s personal position, especially around residency in Spain and the wider personal planning that follows a move.

Practical point

A tax-efficient Irish company on paper can become a poor fit if the owner is already living and running the business in Spain. In many cases, the compliance burden grows before the tax savings do.

The first issue: Where are you a tax resident?

Planning your move to Spain?

Before relocating, it is worth reviewing your visa options alongside your tax position. Explore the application process for Spain’s digital nomad visa or understand the requirements for a Spanish non-lucrative visa.

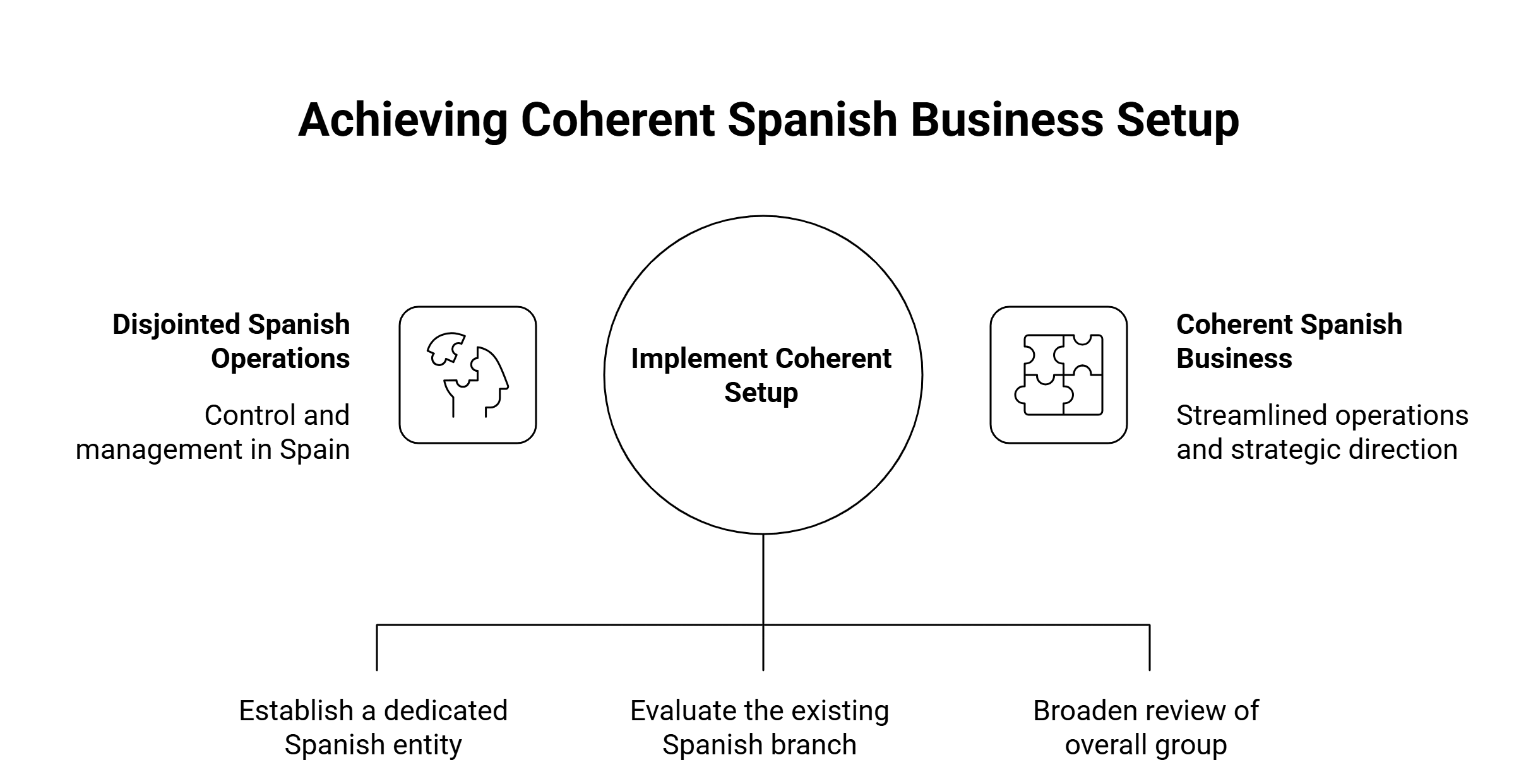

The second issue: Where is the company really managed?

Company residence is another central part of tax structuring between Ireland and Spain. Revenue states that a company incorporated in Ireland on or after 1 January 2015 is deemed tax resident in Ireland, unless a double taxation agreement treats it as resident elsewhere. Revenue also explains that a foreign-incorporated company that is centrally managed and controlled in Ireland can be an Irish tax resident. This is exactly why an Irish company cannot be assessed only by its certificate of incorporation. If real board control, strategic direction and commercial management shift to Spain, the business may need a more coherent Spanish setup, whether through a new Spanish company, a branch analysis or a broader review of group structure.

For businesses that are already comparing legal and tax frameworks, our guide to Spanish corporate tax is a useful next step.

If real board control, strategic direction and commercial management shift to Spain, the business may need a more coherent Spanish setup, whether through a new Spanish company, a branch analysis or a broader review of group structure.

For businesses that are already comparing legal and tax frameworks, our guide to Spanish corporate tax is a useful next step.

Corporate tax is not the whole story

It is easy to reduce tax structuring between Ireland and Spain to a rate comparison, but that approach is too narrow.

Corporate tax comparison

That means a transition should not be driven by the headline rate alone.

The real question is whether the business still has an Irish trading profile with Irish management, or whether a Spanish business model now reflects the facts better.

Ireland

12.5% applies to trading income.

25% applies to certain non-trading income, such as rental and investment income.

Spain

25% is the general corporate tax rate.

15% may apply to certain new entities, but only during specific early periods.

How the Ireland-Spain tax treaty fits in

The tax treaty between Ireland and Spain is an important part of tax structuring between Ireland and Spain. It helps prevent the same income from being taxed twice and sets clear rules for how cross-border income is treated. For example, dividends paid between the two countries may be taxed at a reduced rate, and in some cases, they may even be exempt if certain conditions are met. The treaty also allows tax paid in one country to be credited against tax in the other, which can reduce the overall tax burden. However, the treaty does not fix a structure that no longer reflects how the business actually operates. If the company and its owner are effectively based in Spain, the overall structure still needs to be reviewed. For more details on how these agreements work in practice, see our guide to UK-Spain double taxation.Final thoughts

Good tax structuring between Ireland and Spain is not about chasing whichever country looks cheaper in a single table. It is about matching the structure to the real business model, the owner’s residence, the company’s management and the treaty framework that sits between both countries.Professional support for tax structuring between Ireland and Spain

Contact Delaguía y Luzón today for tailored advice on tax structuring between Ireland and Spain, including company restructuring, tax residency, and cross-border compliance.- Email: felix.delaguia@delaguialuzon.com

- Phone: +34 963 74 16 57