Key takeaways

- The VAT exemption regime for autónomos in Spain allows qualifying small businesses to operate without charging VAT, reducing administrative obligations.

- Eligibility depends on turnover thresholds (around €85,000) and specific criteria, and the regime must usually be opted into rather than applied automatically.

- Foreigners and expats with cross-border activities may still face VAT obligations (e.g. reverse charge or EU rules), making professional advice essential before applying.

Autónomo VAT exemption Spain: What foreigners and self-employed professionals should know

If you are self-employed, or planning to move your business to Spain, you may have heard that some autónomos can benefit from VAT exemption Spain.

This topic has created a great deal of confusion, especially among foreigners, digital nomads, and small business owners trying to understand whether they can legally invoice without IVA in Spain.

Is there a new tax regime for self-employed and small businesses?

The starting point is important: under Spain’s current VAT system, there has traditionally not been a broad domestic turnover-based exemption for autónomos simply because they are small.

In practice, most self-employed professionals carrying out taxable activities in Spain must register correctly, issue compliant invoices, charge VAT where required, and file the relevant VAT returns with the Spanish Tax Agency.

What has changed is the legal framework at the EU level for a special scheme for small enterprises, which Member States must transpose into national law.

For Spain, the practical impact depends on the final wording adopted in national legislation and published in the official rules.

That means foreigners and expats should be cautious: until the Spanish rules are fully in force and clearly regulated, you should not assume that being below a certain turnover allows you to stop charging VAT.

For many international clients, this issue also links to tax residence in Spain, the choice between operating as an autónomo or through a company, and broader cross-border planning such as tax structuring between Ireland and Spain or understanding US and Spanish tax implications.

What the official Spanish framework says today

Spain’s VAT system is governed by Ley 37/1992, de 28 de diciembre, del Impuesto sobre el Valor Añadido, and administered mainly by the Agencia Estatal de Administración Tributaria (AEAT).

Under that framework, VAT generally applies to supplies of goods and services carried out by entrepreneurs or professionals in the course of their business activity.

For most autónomos, the practical consequences have usually included:

- Issuing invoices that meet Spanish invoicing rules;

- Charging VAT where the supply is taxable in Spain and no exemption applies;

- Filing periodic VAT returns, usually through Modelo 303;

- Keeping VAT records and supporting documents; and

- Complying with additional reporting obligations where relevant.

This remains the safest legal starting point for anyone operating in Spain, including foreigners who have moved under a Digital Nomad Visa, a non-lucrative visa, or who later qualify for long-term residence in Spain.

Why are people talking about a new VAT exemption Spain?

The discussion comes from the EU’s reform of the small enterprise rules through Council Directive (EU) 2020/285.

In simple terms, the EU framework allows Member States to create a regime under which a qualifying small business may:

- Issue invoices without charging VAT;

- Avoid some regular VAT reporting obligations; and

- Benefit from a simpler administrative framework.

However, this does not mean that every autónomo in Spain can automatically stop charging IVA.

Spain must adopt and publish its own national rules, including eligibility conditions, entry-into-force rules, and any turnover threshold it chooses to apply within the EU framework.

Who may benefit if Spain implements the small enterprise scheme

If Spain introduces or expands a turnover-based small business exemption, the people most likely to be interested are:

- Freelancers serving private clients in Spain;

- Consultants with low overheads;

- Newly established autónomos with modest turnover;

- Foreign residents testing the Spanish market before incorporating a company; and

- Microbusinesses that value simplicity more than recovering input VAT.

That said, many foreigners will still need a detailed legal and tax review.

A person may be self-employed for Spanish tax and social security purposes, while also dealing with cross-border invoicing, foreign income, permanent establishment risks, or even corporate structuring questions linked to corporate tax in Spain.

Current rules versus a possible small enterprise regime

| Issue | Standard Spanish VAT position | Small enterprise regime if adopted in Spain |

|---|---|---|

| Charging VAT | Usually required where the service or supply is taxable in Spain, and no exemption applies. | Potentially not required for qualifying small businesses, subject to the final Spanish rules. |

| VAT returns | Periodic filing obligations generally apply, commonly through Modelo 303. | May be reduced or simplified, depending on how Spain implements the regime. |

| Deducting input VAT | Normally possible where legal requirements are met and the expense is linked to taxable business activity. | Usually restricted or unavailable under exemption-style schemes. |

| Administrative burden | Higher, with invoicing, accounting and filing obligations. | Potentially lower, but not necessarily simple for cross-border activity. |

| Best suited to | Businesses that need to recover VAT or operate regularly with business customers. | Low-cost, small-scale businesses that prioritise simplicity and do not rely on input VAT recovery. |

When the new regime may and may not help

Indicative suitability chart

Likely to benefit if eligible

Needs a cost-benefit review

Often still VAT-complex

This chart is illustrative only. Actual eligibility and tax efficiency depend on the final Spanish rules, the place of supply, your customer profile, and whether you need to recover input VAT.

Why foreigners should be especially careful

Many foreign entrepreneurs assume that a small business exemption works in the same way across Europe.

It does not. Spain has its own domestic VAT law, its own invoicing rules, and its own interaction between VAT, personal tax residence, company law, and social security status.

Foreigners are often affected by additional issues, such as:

- Whether they are genuinely resident in Spain for tax purposes;

- Whether they carry on the activity personally or through a foreign company;

- Whether Spanish source income is being generated;

- Whether the business has a fixed establishment in Spain;

- Whether the clients are private individuals or businesses, and

- Whether the services fall under place-of-supply rules that shift VAT treatment.

That is why a person moving to Spain under a remote-work arrangement should not only ask about VAT.

They should also check residence, personal income tax, social security, and immigration status.

This is particularly relevant for those considering a Spain Digital Nomad Visa as a W-2 employee or those who are becoming self-employed in Spain.

When an autónomo in Spain may already invoice without VAT

It is also important not to confuse the new small enterprise regime with situations in which an invoice may already be issued without Spanish VAT under the existing rules.

Depending on the activity, examples may include:

- Specific exempt services provided under the VAT Act;

- Certain education, health, or financial activities where the exemption requirements are met;

- B2B services are subject to the reverse charge mechanism because the place of supply is outside Spain, or

- Other transactions not subject to Spanish VAT because the taxable event takes place elsewhere.

In those cases, the invoice may be issued without Spanish VAT for a legal reason that already exists under current law.

That is not the same as saying the autónomo is generally exempt from VAT because the business is small.

What happens to input VAT if you do not charge VAT

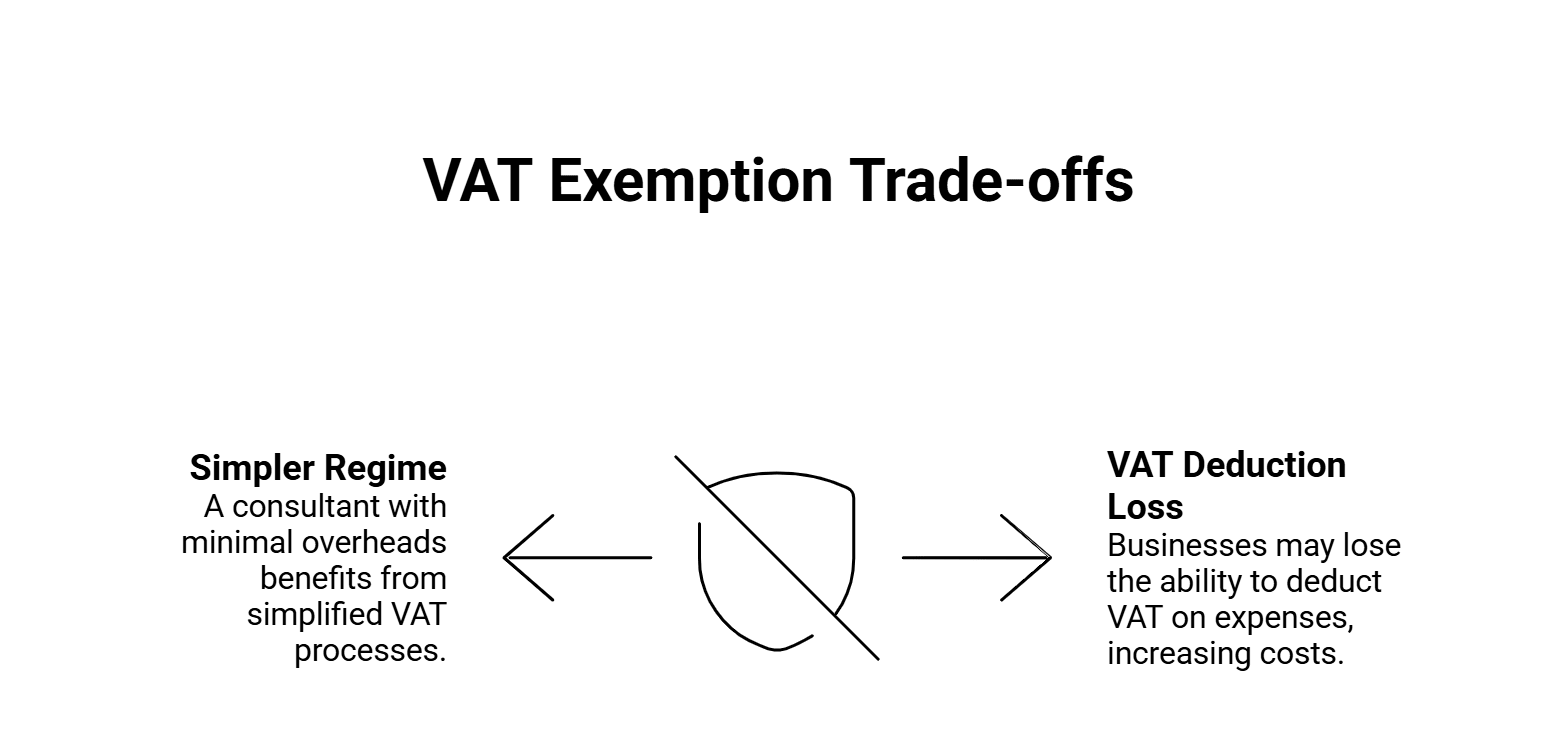

One of the most important practical points is that exemption-style schemes usually come with a trade-off: if you stop charging VAT, you may also lose the right to deduct VAT on business expenses.

This matters far more than many small businesses realise.

A consultant with almost no overheads may welcome a simpler regime.

By contrast, a business that pays significant VAT on rent, equipment, professional subscriptions, subcontractors, or software may be worse off overall.

Cross-border activity can still keep VAT complicated

For foreigners in Spain, the biggest trap is assuming that a domestic simplification removes cross-border VAT issues. It may not.

Even where a simplified domestic regime exists, the following questions can still matter:

- Are your customers businesses or consumers?

- Are they in Spain, another EU country, or outside the EU?

- Are you providing general consulting services, digital services, training, property-related services, or goods?

- Do the invoices need reverse charge wording?

- Do you have obligations connected to intra-EU transactions?

This is why the VAT position should be reviewed together with your wider tax structure by a professional Spanish accountant.

Professional support for autónomos and VAT in Spain

Contact Delaguía y Luzón today for tailored advice on

VAT exemption Spain for autónomos, including eligibility, tax optimisation, and compliance for foreigners and expats.

- Email: felix.delaguia@delaguialuzon.com

- Phone: +34 963 74 16 57