Key takeaways

- The Spain exit tax may apply when individuals with significant shareholdings or investments change their tax residency and leave Spain.

- The tax targets unrealised capital gains on shares or equity holdings, meaning gains may be taxed even if the assets have not been sold.

- Proper planning, including reviewing tax residency in Spain and analysing potential double taxation issues, can help reduce unexpected liabilities.

Leaving Spain? Here’s how the Spain exit tax could affect your assets

Spain has become an attractive destination for entrepreneurs, digital professionals, and investors.

However, individuals with significant investments or business ownership should be aware of an important rule before relocating abroad: the Spain exit tax.

The Spanish exit tax is designed to prevent high-net-worth individuals from moving abroad simply to avoid capital gains taxation.

If certain conditions are met, Spain may tax unrealised gains on shares or financial assets when a taxpayer leaves the country.

This rule mainly affects founders, investors, crypto holders, and individuals with substantial portfolios.

Understanding how it works helps avoid unexpected tax liabilities and plan properly before relocating.

If you are considering moving abroad, it is also important to review the requirements for residency in Spain and how tax obligations change once you stop being a Spanish tax resident.

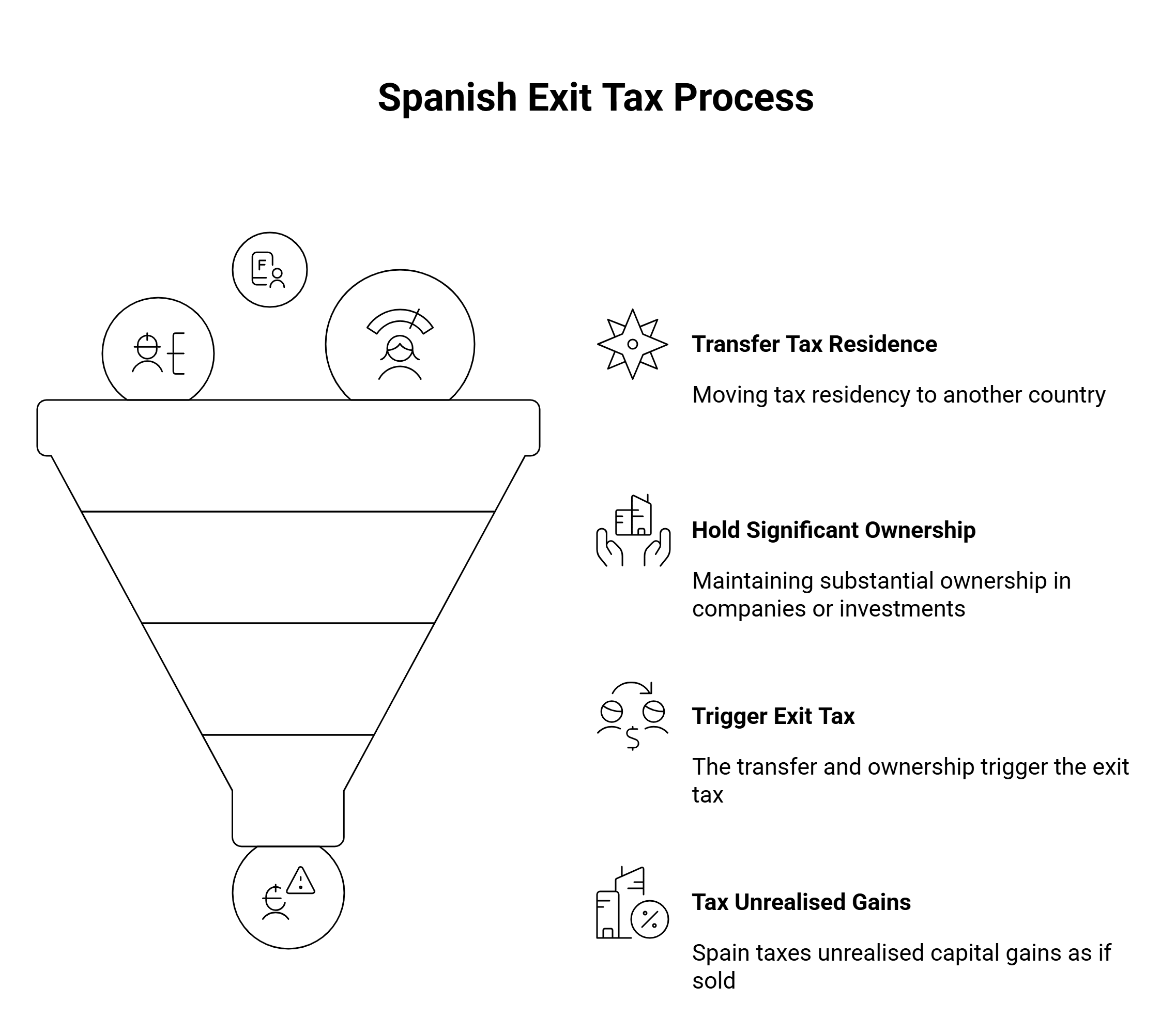

What is the Spain exit tax?

The Spain exit tax is regulated under Article 95 bis of the Spanish Personal Income Tax Law (Ley del IRPF).

It applies when a Spanish tax resident transfers their tax residence to another country while holding significant ownership in companies or financial investments.

When the exit tax applies, Spain taxes the unrealised capital gains on shares and certain financial assets as if they had been sold at the time of departure.

This means the Spanish Tax Agency (Agencia Tributaria) calculates the difference between the assets’ acquisition value and market value as of the day residency changes.

Who must pay the exit tax in Spain?

Not every departing resident is subject to this tax.

It generally applies when both residency and asset thresholds are met.

| Condition | Requirement |

|---|---|

| Spanish Tax Residency | You must have been a Spanish tax resident for at least 10 of the last 15 years |

| Shareholdings Value | Total value of shares exceeds €4 million |

| Ownership in a Single Company | If holdings exceed €1 million in one company and ownership is at least 25% |

These thresholds mean that the tax typically affects:

- Startup founders relocating abroad

- Investors with large equity portfolios

- Entrepreneurs selling businesses after moving

- High-net-worth individuals changing tax residency

For entrepreneurs considering relocating or expanding their business structure, it may also be useful to review the legal framework around Spainish corporate tax and international business planning.

How the exit tax is calculated

The Spanish tax authority calculates the tax based on the unrealised gain of the shares or participations held by the taxpayer.

The formula is simple:

Exit Tax = Market Value – Acquisition Value

The resulting gain is taxed under the Spanish savings income tax rates.

| Capital Gain | Tax Rate (Spain) |

|---|---|

| Up to €6,000 | 19% |

| €6,000 – €50,000 | 21% |

| €50,000 – €200,000 | 23% |

| €200,000 – €300,000 | 27% |

| Over €300,000 | 28% |

This means that even though the shares are not sold, the tax authority treats the departure as a taxable event.

Can the exit tax be deferred?

Spain allows deferral in certain cases, particularly when the individual moves to another EU or EEA country.

Under EU freedom of movement rules, taxpayers may defer payment until:

- The shares are actually sold

- The taxpayer moves outside the EU

- Ownership of the shares changes

However, the taxpayer must still declare the exit tax when leaving Spain and comply with administrative requirements.

International tax planning can significantly reduce the risk of double taxation, especially for individuals with cross-border income, such as UK residents.

For a deeper understanding of cross-border taxation rules, read our guide on

UK–Spain Double Taxation

.

Exit tax and cryptocurrency Investors

While the Spanish exit tax primarily targets shares and equity holdings, crypto investors should still pay attention.

If cryptocurrencies are held through corporate structures, investment vehicles, or tokenised equity instruments, exit tax rules may indirectly apply.

Additionally, crypto gains realised before leaving Spain remain subject to Spanish capital gains tax.

For investors considering relocating for tax purposes, it is essential to evaluate strategies to reduce your tax burden in Spain legally before changing residency.

Exit tax comparison: Spain vs other countries

Several countries apply similar “departure tax” rules to prevent tax avoidance.

However, the thresholds and mechanisms vary significantly.

| Country | Exit Tax Exists? | Main Trigger |

|---|---|---|

| Spain | Yes | Shares above €4M or €1M with 25% ownership |

| United States | Yes | Applies to “covered expatriates” with net worth over $2M |

| Canada | Yes | Deemed disposition of assets when leaving |

| Australia | Yes | Capital gains are triggered when ceasing tax residency |

| United Kingdom | Limited | Temporary non-residence rules on certain gains |

For individuals with US citizenship or assets connected to the United States, tax obligations can be particularly complex.

To better understand cross-border tax obligations, explore our guide on US and Spanish Tax Implications, which explains how both systems interact.

Example scenario: Startup founder leaving Spain

Consider an entrepreneur who founded a technology startup in Spain.

- Initial investment: €50,000

- Current valuation of shares: €3 million

- Tax residency in Spain for 12 years

If the founder moves abroad, Spain may consider that the shares have been “sold” at market value.

The taxable gain would be:

€3,000,000 – €50,000 = €2,950,000 capital gain

This gain would then be taxed under Spain’s savings tax rates, potentially resulting in a substantial tax liability even without selling the shares.

This is why many founders seek professional advice before relocating or restructuring ownership.

Final Thoughts

The Spain exit tax is an important rule for entrepreneurs, investors, and high-net-worth individuals considering leaving the country.

Although Spain offers many attractive opportunities for business and investment, departing residents with significant shareholdings must carefully review the tax consequences of relocating.

With proper legal and tax planning, it is possible to manage exit tax exposure while remaining compliant with Spanish regulations and international tax treaties.

If you are planning to move abroad or restructure your investments, obtaining specialised advice can help ensure a smooth transition and avoid unexpected tax liabilities.

Professional legal support for Spain exit tax planning

Contact Delaguía y Luzón today to receive clear, strategic advice on Spain exit tax and the legal implications of changing your tax residency.

Our team assists entrepreneurs, investors, crypto holders, and high-net-worth individuals with international tax planning before relocating abroad.

- Email: felix.delaguia@delaguialuzon.com

- Phone: +34 963 74 16 57